IRS TIN Matching Program

Internal Revenue Service (IRS) Taxpayer’s Identification Number (TIN) Matching Program

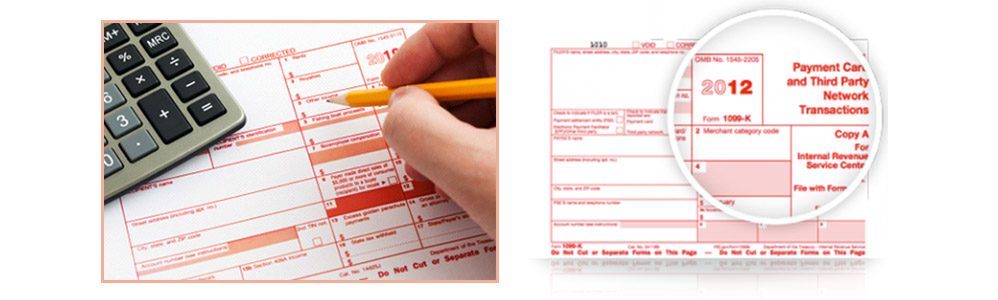

Effective January 2011, all payments made in settlement of payment card transactions are required to be reported under the Federal Housing Assistance Tax Act Section 6050W(IRS Reporting). This requires merchant acquiring entities such as ourselves to file an information return for each calendar year reporting all payment card transactions and third party network transactions with participating payees occurring in that calendar year. This requirement to file information returns applies to returns for calendar years beginning after December 31, 2010. This section also requires statements (1099K) to be furnished to participating payees on or before January 31st of the year following the year for which the return is required.

The Act also amended section 3406(b)(3) to provide that amounts reportable under section 6050W are subject to backup withholding requirements. Section 3406(a)(1) requires certain payers’ to perform backup withholding by deducting and withholding income tax from a reportable payment (as defined in section 3406(b)(1)) if the payee fails to furnish the payee’s taxpayer identification number (TIN) to the payer on a required return, or if the Secretary notifies the payor that the TIN furnished by the payee is incorrect. Backup withholding for amounts reportable under section 6050W applies to amounts paid after December 31, 2011.

What does this mean for you?